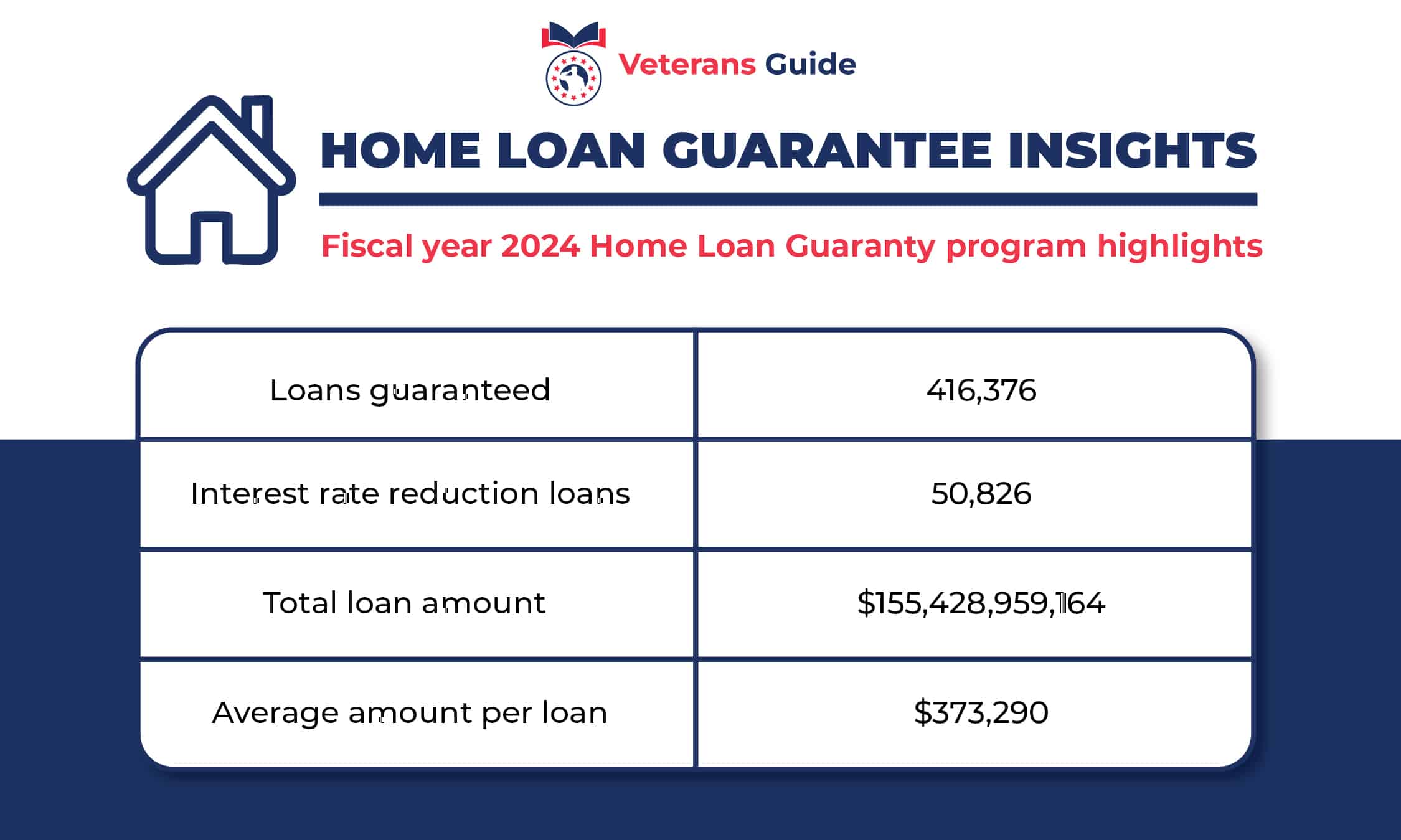

VA Home Loans

Are you ready to purchase or refinance a home? Are you currently in the military or a veteran? If so, you may qualify for a VA home loan. The benefits of VA home loans surpass conventional loans, making it easier for the brave men and women of the military to achieve the dream of owning a home.

Disclaimer: Paid advertising. We receive advertising fees from Novus Home Mortgage.

As a veteran, you have unique opportunities for home financing. The VA home loan program is designed to help you achieve your homeownership dreams. VA home loans help service members, eligible surviving spouses, and veterans buy, repair, or keep homes.

VA home loans offer several advantages for military members. You can receive favorable qualifying terms, including little or no money down and lower required credit scores.

Buying a home is an exciting time in a person’s life, but make sure you have all the facts and explore your options before making such a big decision. Knowing what to expect and the application process will help you have confidence as you move forward.

VA loans offer significant advantages, making homeownership more accessible and affordable for veterans and active-duty service members.

Jodi Ulrich

Mortgage - NMLS#9456

What Is a VA Home Loan?

When purchasing a house, most people apply for a conventional loan. A VA home loan is unique. It’s backed by the government and sponsored by the U.S. Department of Veterans Affairs, which guarantees the loans.

A VA home loan limit is not a limit on the loan you can receive, but rather a cap on the amount the VA will guarantee to your lender. Contrary to what some may believe, the Department of Veterans Affairs does not directly lend money to VA Home Loans. Instead, private lenders such as banks, mortgage companies, and credit unions finance the loan while the VA guarantees a portion of the loan amount.

This guarantee gives lenders the confidence to offer more favorable terms since the VA backs a part of the loan should the borrower default. However, the VA does determine who qualifies.

Types of VA Home Loans

The VA home loan program offers a wide variety of options, including the following:

- VA Purchase Loan: These are designed to help veterans purchase homes at competitive interest rates with no down payment and no private mortgage insurance, or PMI.

- VA IRRRL: Also known as the Interest Rate Reduction Refinance Loan, this option allows you to refinance your existing VA loan at a lower interest rate, potentially reducing your monthly mortgage payments and saving you money over time.

- VA Cash-Out Refinance: This loan is for you if you want to take cash out of your home’s equity. It enables you to refinance a non-VA loan into a VA loan and extract cash for any purpose, whether home improvement or debt consolidation.

- VA Energy Efficient Mortgage: This add-on to your VA home loan facilitates financing energy-efficient improvements to your home. It’s an excellent choice for veterans aiming to make their homes eco-friendly while saving on energy costs.

- Native American Direct Loan: If you’re a veteran and you or your spouse is Native American, the VA’s Native American Direct Loan, or NADL, program may help you get a loan to buy, build, or improve a home on federal trust land.

- VA Renovation Loan: A VA renovation loan allows eligible veterans and active-duty service members to purchase or refinance a home and finance repairs or upgrades to their homes with no down payment or private mortgage insurance.

- VA Jumbo Loan: VA jumbo loans allow veterans to purchase homes that exceed standard price limits, often with $0 down payment up to $1.5 million or more. These loans provide financing for properties in high-cost areas without requiring private mortgage insurance.

Each loan serves a different purpose, catering to various needs and preferences. Assess your circumstances to choose the option that aligns perfectly with your home-ownership goals.

Ready to Start? Calculate Your VA Home Loan Mortgage Payment

Legal Framework for VA Home Loans

Qualified borrowers can use the VA home loan for several purposes. These include the following:

- Purchasing an existing, move-in-ready home

- Purchasing a single-family home

- Purchasing a VA-approved condo or townhouse

- Purchasing a multi-unit property with up to four units if the borrower resides in one unit full-time

- Purchasing a mobile or manufactured home

- Refinancing your home, available with the VA cash-out refinance

Understanding what you can and cannot do with the loan helps avoid disappointments or mistakes.

Benefits of a VA Home Loan

The VA home loan program, administered by the U.S. Department of Veterans Affairs, offers an array of benefits designed to help veterans purchase a home with greater ease and fewer restrictions.

Zero Down Payment

One of the standout benefits of a VA home loan is the possibility of financing 100 percent of the home’s value, meaning you can buy a home with no down payment. This is a substantial financial relief, especially if you’re looking to establish roots but haven’t had the chance to build your savings.

No Private Mortgage Insurance

Conventional loan borrowers who cannot make a 20 percent down payment must purchase private mortgage insurance, or PMI, which can drastically increase their monthly payments. VA home loan borrowers are exempt from this requirement.

The average cost of PMI for conventional loans ranges from 0.46 percent to 1.50 percent of the original loan amount per year. Being exempt from this can help home buyers save tens of thousands of dollars over the life of their loan.

Refinancing

Refinancing with a VA Home Loan offers many advantages for eligible veterans and active-duty service members. Most notably, the VA Interest Rate Reduction Refinance Loan, or IRRRL, facilitates a streamlined process, often with reduced documentation and no appraisal.

Refinancing with an IRRRL leads to potentially lower interest rates, saving thousands over the loan’s lifespan. Additionally, no out-of-pocket costs, and the option to roll fees into the loan makes the process financially easier.

Competitive Interest Rates

VA Home Loan rates have historically been more favorable than conventional mortgage rates. On average, VA rates are about 0.25 percent to 0.50 percent lower than conventional rates over the years. Several factors have narrowed the gap between VA and conventional loan rates, including fluctuations in economic conditions, market demand, and conventional loan risk factors.

Potential borrowers should note that while rates may be similar, the absence of PMI, more lenient credit requirements, and the lack of down payments make VA loans a more appealing option for eligible individuals.

First-time buyer or seasoned homeowner: the VA loan is designed to evolve with your journey.

Jodi Ulrich

Mortgage - NMLS#9456

How Do VA Loans Compare to Traditional Loans?

| VA Loans | Conventional Loans | FHA Loans | |

|---|---|---|---|

| Down Payments | No down payment | Down payment required | Lower down payments than conventional loans |

| Private Mortgage Insurance | No PMI required | PMI required | PMI required |

| Interest Rates | Competitive, lower interest rates | Generally, higher interest rates | Competitive |

| Qualification | Less stringent than typical loan requirements | Stricter credit score and income requirements | Allows lower credit scores and higher debt-to-income ratios |

| VA Loans | |

|---|---|

| Down Payments | No down payment |

| Private Mortgage Insurance | No PMI required |

| Interest Rates | Competitive, lower interest rates |

| Qualification | Less stringent than typical loan requirements |

| Conventional Loans | |

|---|---|

| Down Payments | Down payment required |

| Private Mortgage Insurance | PMI required |

| Interest Rates | Generally, higher interest rates |

| Qualification | Stricter credit score and income requirements |

| FHA Loans | |

|---|---|

| Down Payments | Lower down payments than conventional loans |

| Private Mortgage Insurance | PMI required |

| Interest Rates | Competitive |

| Qualification | Allows lower credit scores and higher debt-to-income ratios |

How to Qualify for a VA Home Loan

Securing a VA home loan involves meeting criteria outlined by the VA, most of which are less stringent than typical loan requirements. The VA will evaluate a veteran’s service requirements, credit score, income, and property type, to name a few.

Service Requirements

The VA makes its loans available only to those who meet one of the following criteria:

- Active Duty Service Members typically qualify after 90 days of continuous service during wartime or 181 days during peacetime.

- Veterans are eligible depending on when and where they served, but generally, those who served at least 90 days of active duty during wartime or 181 days during peacetime meet the criteria. Service requirements also differ depending on when you served.

- National Guard and Reservists usually qualify after six years of service. However, those mobilized for active duty may be eligible sooner.

- Surviving Spouses may qualify if they haven’t remarried and their service-member spouse died in the line of duty or due to a service-related disability.

Credit Score

Your credit score is pivotal in determining your eligibility for a VA home loan. Maintaining a healthy credit score is advisable, as lenders often offer more favorable terms to borrowers with good credit histories. While the VA doesn’t set a minimum credit score, most lenders look for a score of at least 620.

Income Stability

Of course, even with all of the VA’s loan benefits, it’s still necessary to have a stable income. Lenders will scrutinize your debt-to-income ratio, or DTI, which compares your gross monthly income to your monthly debt payments. A lower ratio indicates better financial stability, increasing your chances of approval.

The acceptable DTI ratio is 41 percent.

To determine your debt-to-income ratio, calculate the money spent on house maintenance, insurance premiums, educational loans, credit cards, car loans, taxes, etc. After that, determine what you earn each month. For example:

- Annual income: $60,000

- Divide by 12 for your monthly income: $60,000 / 12 = $5,000

- Multiply your monthly income by 0.41: $5,000 x 0.41 = $2,050

In this example, if your monthly debt payments are $2,050 or less, you can qualify for a VA home loan.

Property Eligibility

VA home loans are designed for primary residences only. Borrowers are expected to occupy the property within 60 days of closing and use it as their primary residence. If the property doesn’t meet this specification, the VA will deny your loan request.

Adhering to these stipulations will smooth out your VA home loan acquisition process while providing you with favorable terms for your dream home. At Veteran’s Guide, you can find information and resources to help you qualify for this loan.

What is a Certificate of Eligibility?

Veterans must obtain a Certificate of Eligibility, or COE, to prove their eligibility for a VA home loan to lenders. A COE is a document that verifies you meet the VA Home Loan requirements. Acquiring a COE usually requires discharge papers, service records, or a statement of service signed by your personnel officer or unit commander.

You can find the COE, VA Form 26-1880, online through the VA’s website or a VA-approved lender.

Financial setbacks happen; the VA loan ensures they don’t have to be permanent.

Jodi Ulrich

Mortgage - NMLS#9456

Can I Use a VA Loan More Than Once?

Absolutely. Veterans and eligible service members can use the VA Home Loan benefit multiple times. However, certain circumstances and conditions can affect how this process works. However, a few circumstances may affect acquiring a VA home loan multiple times.

First Home vs. Subsequent Homes

Generally, there’s no difference in the interest rates offered for first-time or subsequent uses of the VA Home Loan. However, the funding fee may vary.

First-time VA loan users typically enjoy a lower funding fee than subsequent users. This fee might be higher if you use the VA loan benefit for the second or third time unless you make a significant down payment.

Selling and Moving to a New Home

If you’ve paid off your first VA loan entirely and have sold the property, you can have your full VA loan entitlement restored to purchase another home with no down payment.

If you retain the first property, perhaps to rent out, and haven’t paid off that VA loan, it might be possible to use your remaining partial entitlement for another purchase. However, depending on the county loan limits and remaining entitlement amount, this might require a down payment.

Home Improvement Loans

If you have an existing VA loan, you can still apply for another VA loan specifically for home improvements, known as the VA Renovation Loan.

This loan allows veterans to finance the purchase and improvement of a home or refinance an existing VA loan to include improvements. The nature and scope of the renovations will be subject to VA approval.

What Is the VA Funding Fee?

The funding fee is a one-time payment on VA Home Loans paid directly to the VA. This fee helps offset the costs to taxpayers by reducing the loan’s overall expense, ensuring the VA Home Loan program remains sustainable for future generations of military veterans.

The funding fee’s cost varies based on several factors:

- Type of Loan: Purchase loans typically have different rates than refinance loans.

- Down Payment: A larger down payment results in a lower funding fee.

- First-Time vs. Subsequent Use: First-time VA loan users usually have a lower fee than subsequent users.

- Military Service Category: Regular military members might have different rates than the Reserves or National Guard members.

Generally, the VA funding fee ranges from 1.4 percent to 3.6 percent of the loan amount. You can pay the funding fee upfront at closing or roll it into the mortgage. It’s important to note that veterans who receive disability compensation from the VA for service-related disabilities are exempt from the VA funding fee, no matter their disability rating.

Disability Exemption Qualifications

Veterans receiving disability compensation from the VA for service-related disabilities are exempt from the funding fee. Any percentage of officially recognized service-connected disability would suffice to qualify.

Applying for a VA Home Loan

To get started with applying for a VA Home Loan, the first step will be to get a Certificate of Eligibility from the VA, which you can apply for via the VA’s website, through your lender, or by mail.

Next, the lender will review your personal information, such as your income and credit history, to evaluate you as a borrower. If they approve your loan, then they will work with you to complete the necessary steps to finalize the purchase and move into your new home.

VA Home Loan FAQs

What Is the VA Guaranty?

With the VA guaranty, the federal government backs a portion of a home loan issued by a private lender to an eligible U.S. veteran and service member. This guarantee enables lenders to offer loans with more favorable terms, such as no down payments, no required private mortgage insurance, and competitive interest rates.

Can Surviving Spouses Apply for a VA Loan?

Surviving spouses of eligible service members can qualify for VA home loans if their spouse’s death was related to their service.

Can I Use a VA Loan for New Construction?

Some VA loan options can be used for new construction of a primary residence, though they require working with a VA-approved lender and builder.

Do I Have To Pay for Closing Costs?

Generally, veteran borrowers are responsible for most closing costs when purchasing a home with a VA loan. However, the VA home loan program does allow for negotiation with the sellers.

How Long Does it Take to Close a VA Home Loan?

In most cases, it takes between 40 and 55 days to close a VA loan for veterans, service members, and their families when buying a home.

Jodi has over 22 years in home lending, specializes in VA loans, and helping military families achieve homeownership. As a top loan officer at Novus, he’s closed over 9,000 loans across 40 states. Jodi is dedicated to empowering veterans with VA benefits, fostering long-term financial success, and offering personalized service.